摘要:

交易员,能不能被系统性培养?4月11日EagleTrader长沙公司落地,给这个行业难题交出了新的答案。同日,「长沙老鹰一飞冲天开业盛典暨自营生态发展峰会」在长沙拉开帷幕,政府代...

摘要:

交易员,能不能被系统性培养?4月11日EagleTrader长沙公司落地,给这个行业难题交出了新的答案。同日,「长沙老鹰一飞冲天开业盛典暨自营生态发展峰会」在长沙拉开帷幕,政府代...

交易员,能不能被系统性培养?4月11日EagleTrader长沙公司落地,给这个行业难题交出了新的答案。

同日,「长沙老鹰一飞冲天开业盛典暨自营生态发展峰会」在长沙拉开帷幕,政府代表、业界领袖、资深交易员齐聚现场,座无虚席。

长沙公司的成立,并不只是一个简单的考试服务点,而是以“政校企协同创新”的模式,打通交易员训练、实战、职业发展等完整成长路径的全新尝试。

孵化真正具备实战能力的顶尖交易员,是EagleTrader始终深耕的事。而这次长沙,只是开始!

自营考核体系全拆解

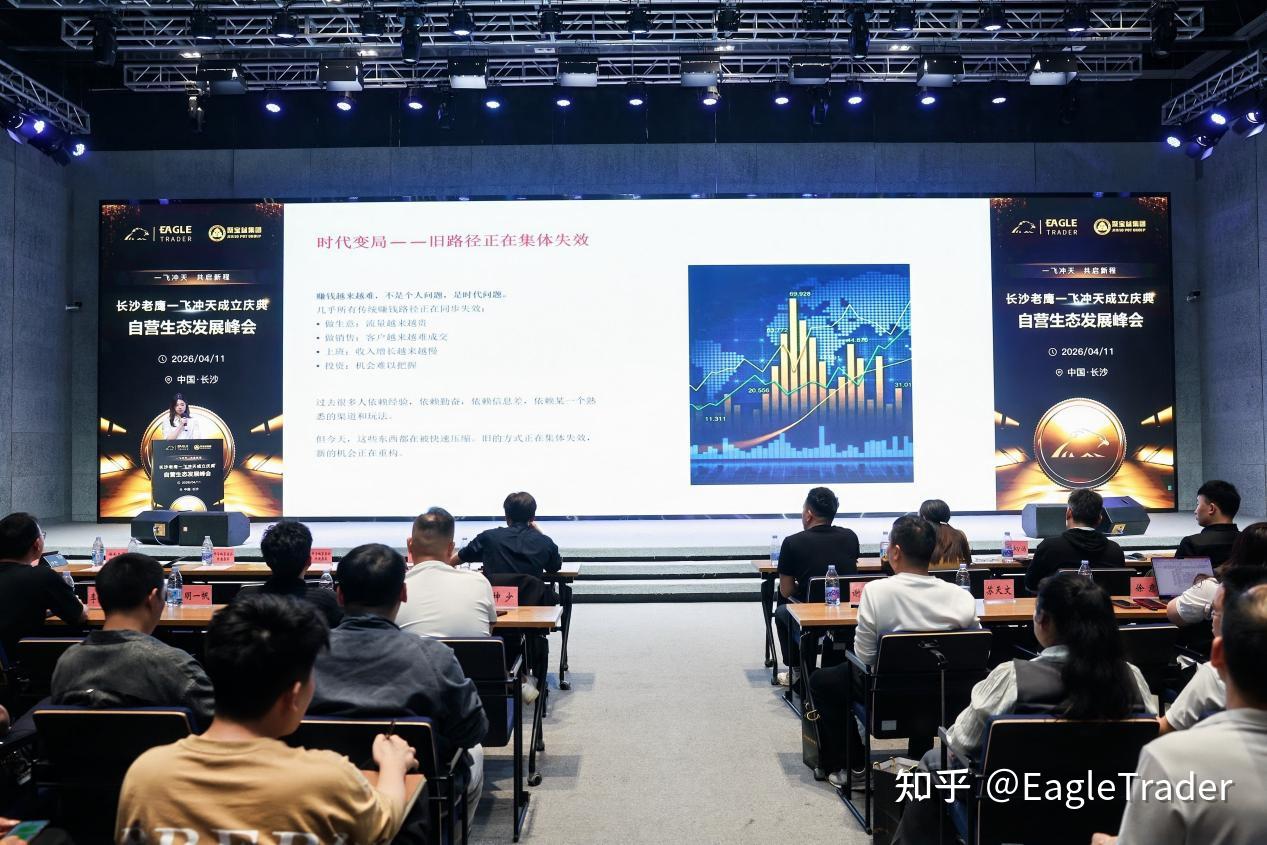

峰会开场,EagleTrader 考试推荐官陈志斌老师,为全场交易者深度解读了自营交易考核体系。

无数交易员困于“有技术没资金”的行业痛点,而这套体系,正是为破解这个难题而生的。

通过两轮标准化考核,全面验证交易员的风险控制能力与稳定盈利能力,考核通过即可直接签约,进入80%利润分成阶段。

这套成熟体系,既能让交易员在标准化训练中养成合规交易习惯、打磨可复制的盈利系统,更能零门槛撬动大额交易资金,彻底摆脱自有资金的束缚,把交易能力直接转化为持续收益。

EagleTrader 全球总监赵明先生在分享中提到,长沙公司的落地,将把这套成熟体系全面下沉内地市场,为交易者提供更便捷、更贴身的考试服务与成长支持,助力更多交易员走出资金困境,实现职业交易破局。

交易员孵化特惠季限时开启

此次峰会为了让更多交易者都能低成本尝试成熟的自营考核体系,踏上体系化成长的快车道,借长沙公司落地的契机,EagleTrader4月重磅开启「交易员孵化特惠季」!

史无前例的优惠力度,线上线下同步开放,新老考生均可参与,用实实在在的支持,陪你解锁职业交易的更多可能。

4月11日 - 4月13日开业狂欢:解锁2张10万、20万正式挑战规模8折优惠券4月14日- 4月21日福利延续:解锁2张10万、20万正式挑战规模8.5折优惠券4月22日 - 4月30日收官福利:解锁3张全规模挑战账户9折优惠券注:每张优惠券只可在相应活动时间内使用,逾期失效!

从入门试水到进阶实战,全规模优惠覆盖适配每一位交易者的成长节奏,消息一经发布,现场氛围瞬间拉满,无数交易者当场报名,抢占入局名额。

实战派亲临峰会现身说法

一套孵化体系行不行,最终还是看真实成长结果说话。本次峰会,多位从EagleTrader成长起来的实战派代表,用亲身经历给出了最有力的答案。

EagleTrader 雄鹰计划首位成员黄欢乐老师,率先分享了自己从普通交易者到职业操盘手的成长历程,拆解了自营体系如何帮交易者避坑、搭建闭环交易系统,实现专业能力的跨越式成长。

ET考生代表袁平、江佳韵、苏天文,也分享了各自在考核体系中的成长收获与实战心得。虽交易理念、操作风格各不相同,但都通过标准化考核实现了稳定盈利突破,也为在场交易者给出了真实的成长指南,现场掌声经久不息。

ET城市合伙人代表陈小花老师,也带来了行业视角的深度分享。其团队深耕交易员孵化培训领域多年,深刻认同 EagleTrader的孵化逻辑,也希望未来能深度携手,共同搭建更完善的交易员成长支持体系,为行业输送更多优秀人才。

ET新手孵化免费赛重磅上线

如果你是刚接触自营交易的新手,怕踩坑、怕试错,还没准备好直接参与正式挑战?那么这场专为新手打造的免费活动,刚好为你而来。

峰会现场,我们同步介绍了近期全新上线的「ET 新手孵化免费赛」,不用你掏一分钱,就能沉浸式体验自营交易的完整模式。

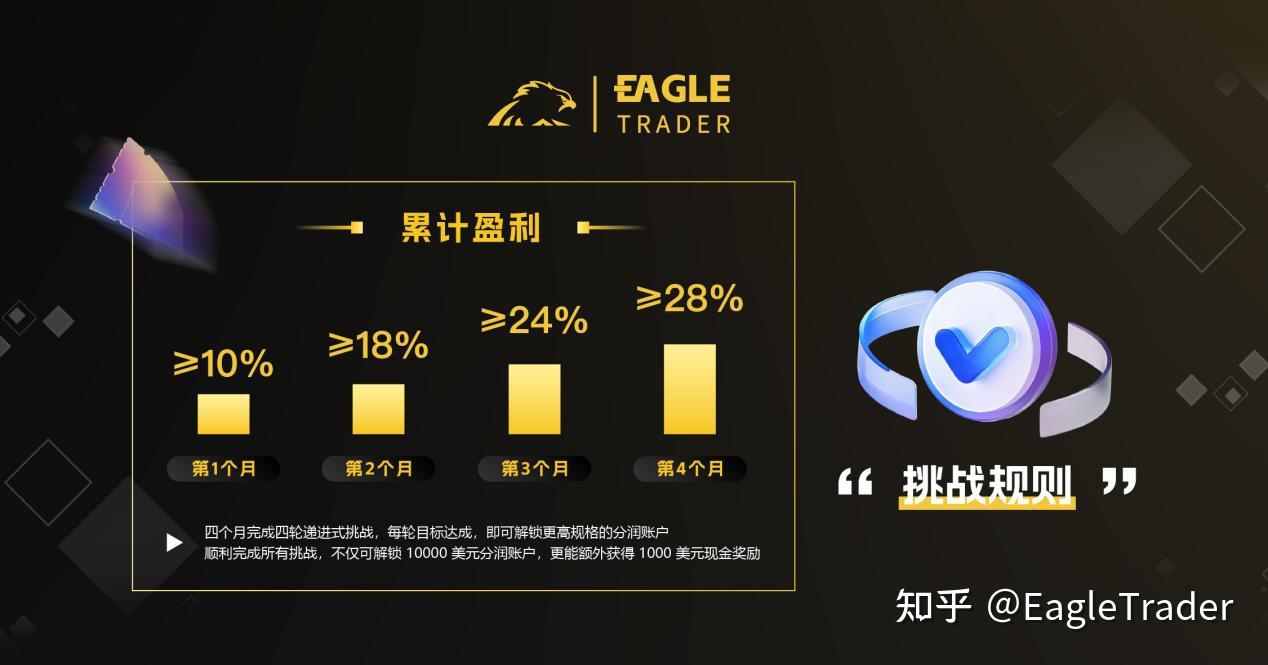

赛账户规模:1000 美元挑战规则:四个月完成四轮递进式挑战,每轮目标达成,即可解锁更高规格的分润账户

3.成长奖励:顺利完成所有挑战,不仅可解锁 10000 美元分润账户,更能额外获得 1000 美元现金奖励

行业大咖圆桌论道

峰会的压轴环节,是以「交易进阶新赛道:自营考核与市场发展机遇」为主题的圆桌论坛。

本次论坛由天恩交易系统创始人坤少主持,金龟量化首席策略师蔡忠晋老师、三生墨交易室联合创始人廖奕墨老师、琦点信息技术咨询创始人陈小花老师、ET40 万美元签约交易员谢纯杰老师同台对话。

围绕自营交易赛道的发展趋势、交易员的系统化成长路径、政校企协同的生态布局等核心议题,畅所欲言,深度碰撞。

现场,各位嘉宾分享了最前沿的市场洞察,拆解了最真实的实战交易策略,为在场的每一位交易者,开辟了全新的交易成长思路与职业发展路径。

论坛结束后,长沙公司启动仪式正式举行,金剪落下,掌声雷动,宣告EagleTrader 长沙公司正式启航。

紧随其后的合伙人签约仪式上,多位合作伙伴现场完成签约,为 EagleTrader自营交易生态建设再添新力,也标志着EagleTrader内地市场的全新篇章正式开启!

长沙公司的落地,不是一次简单的版图扩张,而是EagleTrader赋能中国交易员的又一次全新出发。

我们见过太多交易者,困于资金、困于认知、困于孤独的摸索,空有热爱与天赋,却始终走不出亏损的怪圈。而EagleTrader要做的,就是为每一位心怀热爱的交易者,拆掉门槛,铺平道路,点亮方向。

自营交易的黄金时代正在到来,你准备好,和我们一起,成为下一位顶尖自营交易员了吗?